Python Object-Oriented Programming (OOP): What can we say about US housing price inflation?¶

Introduction¶

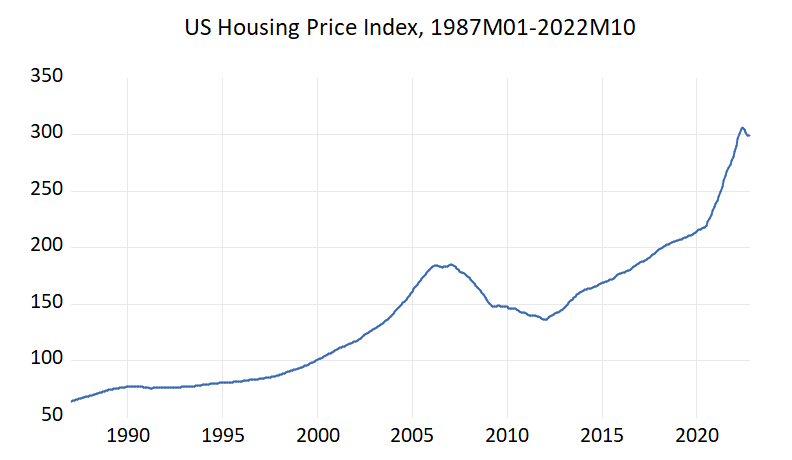

In this project, we analyze housing price inflation in the USA using object-oriented programming (OOP). Our econometric strategy is the autoregressive modeling approach. We use OOP to apply the AR process to a time series data. We consider a housing proce index:

$y_{t}$: S&P/Case-Shiller U.S. National Home Price Index

You can acess this data from https://fred.stlouisfed.org/series/CSUSHPISA. For more information regarding the index, please visit Standard & Poor's (https://www.spglobal.com/spdji/en/documents/methodologies/methodology-sp-corelogic-cs-home-price-indices.pdf). There is more information about home price sales pairs in the Methodology section. Copyright, 2016, Standard & Poor's Financial Services LLC. Reprinted with permission.

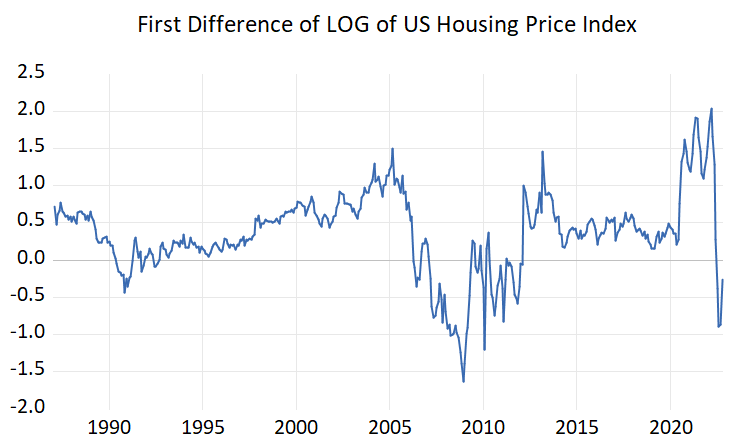

From this figure, also from unit root tests, we understand this variable is nonstationary in level. Thus, we use first difference of LOG = percentage change:

Let's make it the subject of another series of articles that this graphic tells us about the US economy. Now our priority is the processing of AR models with OOP. Let's download the necessary packages:

import numpy as np

import numpy.random as rnd

import matplotlib.pyplot as plt

from numpy import hstack, nan, tile, vstack, zeros

try:

import seaborn

except ImportError:

pass

Defining an AR Class¶

Let's create an AR class and define the methods and basic building blocks within this class.

class AR(object):

def __init__(self, data=None, ar_order=1):

self._data = data

self._ar_order = ar_order

self._sigma2 = 1

self._T = None

self._X = None

self._y = None

self._roots = None

self._abs_roots = None

self._fit_values = None

self._parameters = None

self._errors = None

if data is not None:

self._generate_regressor_array()

@property

def data(self):

return self._data

@property

def ar_order(self):

return self._ar_order

@property

def parameters(self):

return self._parameters

@property

def sigma2(self):

return self._sigma2

@property

def roots(self):

return self._roots

@property

def abs_roots(self):

return self._abs_roots

@property

def fit_values(self):

if self._fit_values is None:

self.estimate()

return self._fit_values

@data.setter

def data(self, value):

self._data = value

self._generate_regressor_array()

if self._parameters is not None:

self._update_values()

@parameters.setter

def parameters(self, value):

if value.ndim not in (1, 2):

raise ValueError("parameters must be a vector")

value = value.ravel()[:, None]

if value.shape[0] != (self._ar_order + 1):

raise ValueError(f"parameters must have {self._ar_order + 1} elements.")

self._parameters = value

self._update_roots()

@sigma2.setter

def sigma2(self, value):

if value <= 0.0:

raise ValueError("sigma2 must be positive")

self._sigma2 = value

def _generate_regressor_array(self):

p = self._ar_order

T = self._T = len(self._data)

x = np.ones((T - p, p + 1))

y = self._data[:, None]

for i in range(p):

x[:, [i + 1]] = y[p - i - 1:T - i - 1, :]

self._y = self.data[p:, None]

self._X = x

def _update_roots(self):

if self._ar_order > 0:

coeffs = self._parameters[1:].ravel()

char_equation = np.concatenate(([1], -1.0 * coeffs))

self._roots = np.roots(char_equation)

self._abs_roots = np.absolute(self._roots)

else:

self._roots = None

self._abs_roots = None

def _update_values(self):

fv = self._X.dot(self._parameters)

e = self._y - fv

self._sigma2 = np.dot(e.T, e) / len(e)

self._errors = vstack((tile(nan, (self._ar_order, 1)), e))

self._fit_values = vstack((tile(nan, (self._ar_order, 1)), fv))

def estimate(self, insample=None):

x = self._X

y = self._y

# y = y[:, None]

p = self._ar_order

if insample is not None:

x = x[:(insample - p),:]

y = y[:(insample - p)]

xpxi = np.linalg.pinv(x)

self.parameters = xpxi.dot(y)

def forecast(self, h=1, insample=None):

tau = self._X[:, 1:].shape[0]

fcasts = hstack((self._X[:, :0:-1], zeros((tau, h))))

p = self._ar_order

params = self._parameters

for i in range(h):

fcasts[:, p + i] = params[0]

for j in range(p):

fcasts[:, p + i] += params[j + 1] * fcasts[:, p + i - (j + 1)]

fcasts = vstack((tile(nan, (p, p + h)), fcasts))

if insample is not None:

fcasts[:insample, :] = nan

return fcasts[:, p:]

def forecast_plot(self, h=1, show=True, show_errors=False):

fcasts = self.forecast(h=h)

T = self._T

p = self._ar_order

aligned = zeros((T + h, 2))

aligned[:T, 0] = self._data

aligned[-T:, 1] = fcasts[:, -1]

aligned = aligned[p:T, :]

fig = plt.figure()

ax = fig.add_subplot(1, 1, 1)

if show_errors:

ax.plot(aligned[:, 0] - aligned[:, 1])

else:

ax.plot(aligned)

if show:

plt.show(fig)

return fig

def hedgehog_plot(self, h=1, show=True, skip=0):

fcasts = self.forecast(h=h)

fig = plt.figure()

ax = fig.add_subplot(1, 1, 1)

ax.plot(self._data)

data = self._data

for i in range(0, self._T, skip + 1):

x = i + np.arange(h + 1)

y = hstack((data[[i]], fcasts[i]))

ax.plot(x, y, 'r')

ax.autoscale(tight='x')

fig.tight_layout()

if show:

plt.show(fig)

return fig

def simulate(self, T=500, burnin=500):

tau = T + burnin + self._ar_order

e = rnd.standard_normal((tau,))

y = zeros((tau,))

p = self._ar_order

for t in range(p, tau):

y[t] = self._parameters[0]

for i in range(p):

y[t] += self._parameters[i + 1] * y[t - i - 1]

y[t] += e[t]

return y[-T:]

Load the data¶

import pandas as pd

housinginf_excel = pd.read_excel("housinginf.xls", skiprows=10,

index_col="observation_date")

# print(gs10_excel)

data = housinginf_excel.housinginf.to_numpy()

We estimate the following model with the estimation and forecasting methods we defined in the AR class: $$y_{t}=\alpha_{0}+\alpha_{1}y_{t-1}+\alpha_{2}y_{t-2}+\alpha_{3}y_{t-3}+\varepsilon_{t}$$

T = 429

ar_order = 3

in_sample = 10

h=5

# Initialize the object

# ar = AR(activity, ar_order)

ar=AR(data,ar_order)

ar.estimate()

forecasts = ar.forecast(h,in_sample)

Let's plot the forecasting error data with the real data:

p = ar_order

aligned = zeros((T + h, 2))

aligned[:T, 0] = data

aligned[-T:, 1] = forecasts[:, -1]

aligned = aligned[p:T, :]

plt.plot(np.arange(1, T-ar_order+1), aligned)

plt.show()

In this figure, the blue series represents the actual data, while the orange series represents the forecast error data. Note: The information in the link below was used in the creation of the OOP for the AR modeling approach: https://www.kevinsheppard.com/teaching/python/notes/#notes